The Unison Difference

The industry calls every offering in this space a home equity investment (HEI). But HEIs and ESAs are fundamentally different, and Unison’s Equity Sharing Agreement stands apart from the rest.

Here's what we do differently:

Unison values your home more accurately

Unison and Point both start by establishing your home’s value with an appraisal and a risk adjustment. Unison's risk adjustment is just 5%. As of July 2026, Point’s typical risk adjustment is 27.5%.

That means that your home’s “starting value” for the home equity investment would be nearly 30% lower than it actually is.

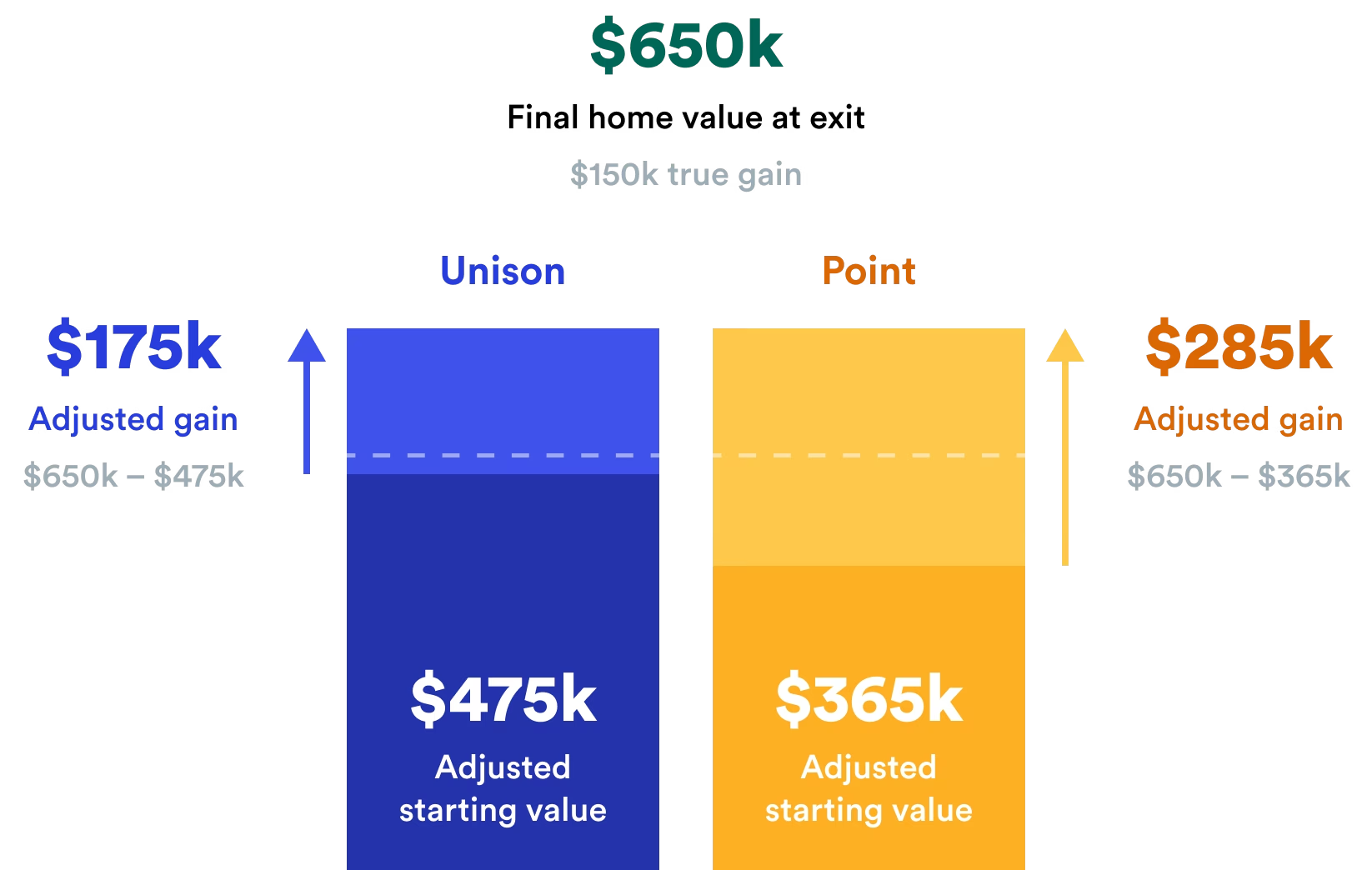

Why? A lower starting value means providers can share in more growth from day one — and less of the downside. For example, imagine your home is appraised at $500,000. With a 27% risk adjustment, your home’s starting value would be just $365,000. Two (big) problems with that:

If your home’s value increases

Let’s say it gets to $650,000 — Point will share in the appreciation. But not from $500,000 to $650,000. From $365,000 to $650,000, which could be a significant cost.

If your home’s value were to decrease

Even with a loss of 10, 15, or even 20% — Point wouldn’t share in any of that downside, since your home is still above $365,000. You’re stuck with depreciation on your home AND paying Point a share of your “profit” above $365,000. Except you didn’t profit at all.

A large risk adjustment means the provider shares more of the upside and less of the downside. Unison's 5% adjustment is transparent from the beginning and keeps our agreement’s starting point more grounded in what your home is actually worth.

Unison has built-in features to help you succeed

We believe in fairness, flexibility, and helping you keep more of the value you create. It’s why we every Unison Equity Sharing Agreement includes these features:

Remodeling Adjustments

Let’s be clear: we both want your home to appreciate in value. Renovations and improvements are a huge part of that, so it’s only fair that you keep the equity that you build with your projects. That’s why Unison offers Remodeling Adjustments.

It means you can document any eligible improvement projects, keep all the records, and when we’re settling up the agreement (as long we’re at least three years in), you can apply to have your improvements appraised. The growth in value they’ve contributed can be carved out from our share, reducing what you owe.

For example, let’s say you use part of your Unison funds to put in a new kitchen. Decades later, when you’re ready to sell, you bring out that folder with your receipts. If the appraiser determines that your upgrades added $40,000 to your home’s value (important: not what they cost to install, but what they added to your home’s value), that $40,000 will be subtracted from your ending value, meaning we don't share in that growth and you keep more of your sale price in your pocket.

Point does not offer any remodeling adjustment. If you improve your home and boost its value, they share in it — no matter what. Suddenly, renovating and improving the place you live can feel like a punishment.

Flexible Options

We know life can be unpredictable, so we work to keep things flexible. That’s why Unison offers early termination options. That means you can always sell your home or settle the agreement at any time. Just keep in mind that some features, like downside sharing, only become available after several years. Point offers the same, but with a larger risk adjustment to share in more appreciation.

Unlike Point, Unison offers partial buyout options. That means we can work with you to accept a partial payment to reduce our share in your equity, without ending the agreement entirely. With Point, that’s not an option: you can only settle the agreement with a lump-sum payment.

Both of these options exist to help support you on your journey as a homeowner. Our goal is not to take all of your appreciation, but to invest in your home alongside you for as long as you need it — and not a moment longer.

Clear Terms

With an Equity Sharing Agreement, you’ll pay a 3.9% origination fee, the cost of the appraisal, and basic closing costs, all clearly presented from the beginning. We also pride ourselves on honest, human customer service. You’ll have a dedicated home equity expert by your side to answer any questions — while you decide, through the signing process, and beyond

Point charges a processing fee of 3.9% (with a minimum of $2,000), plus standard third-party closing costs, which can include government recording fees and other costs, which should be reviewed in closing disclosures.

Unison discloses its origination fee and standard closing costs clearly upfront.

Loss Sharing

As you now know, oversized risk adjustments allow HEI companies to “say” they’ll share in the downside with you — but rarely actually have to.

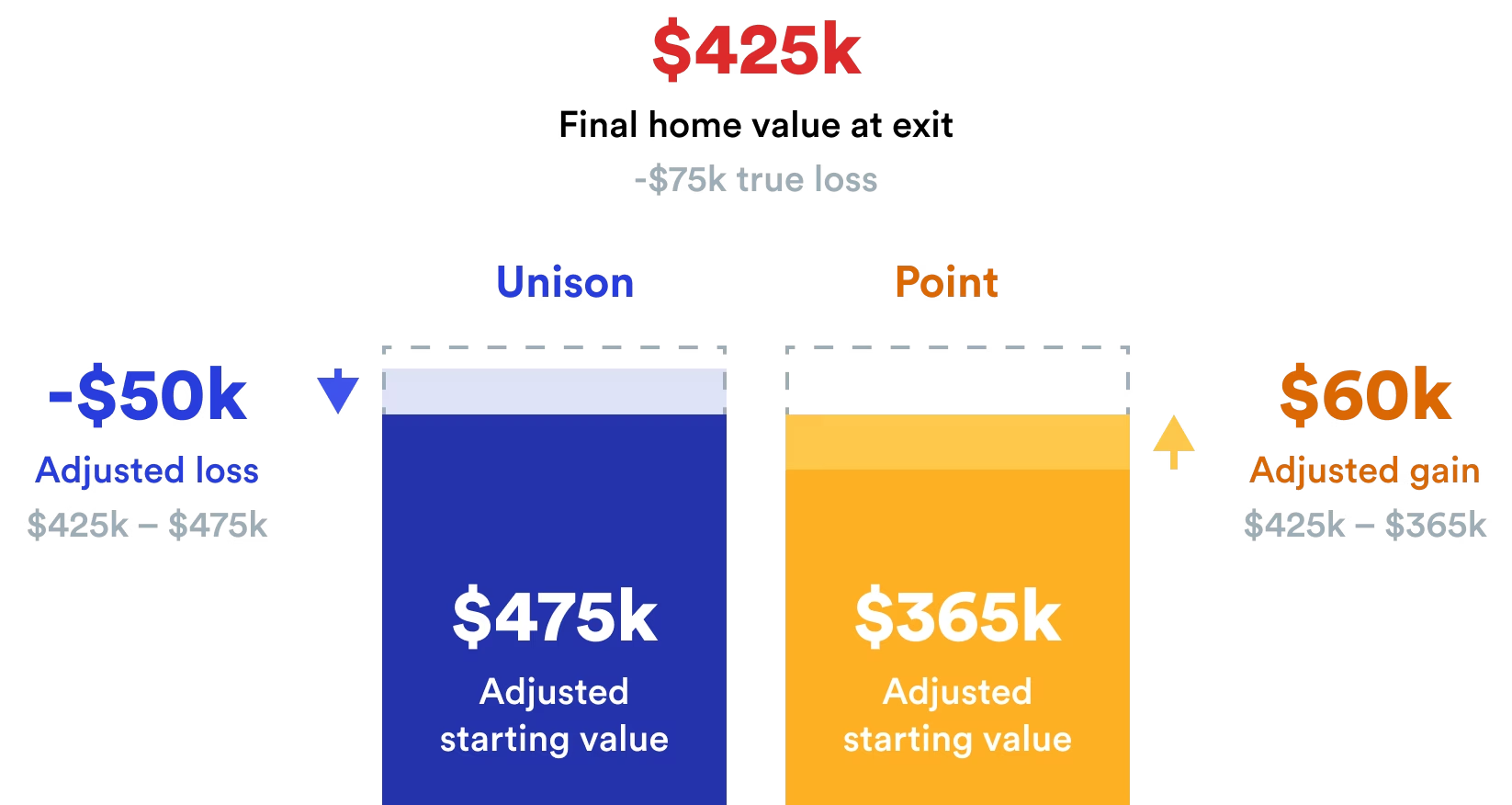

To demonstrate the difference, here’s a closer look at the example from above, where the home depreciated by 15%. With Unison, we'd share in a significant portion. Our hypothetical homeowner unlocked $50,000, and at the end, only needs to return $30,000 to Unison.

With Point, even when the home depreciates the same amount, the home is actually considered to be worth more than at the adjusted starting value. Our hypothetical homeowner unlocked $50,000, and at the end, would pay Point as much as $67,000.

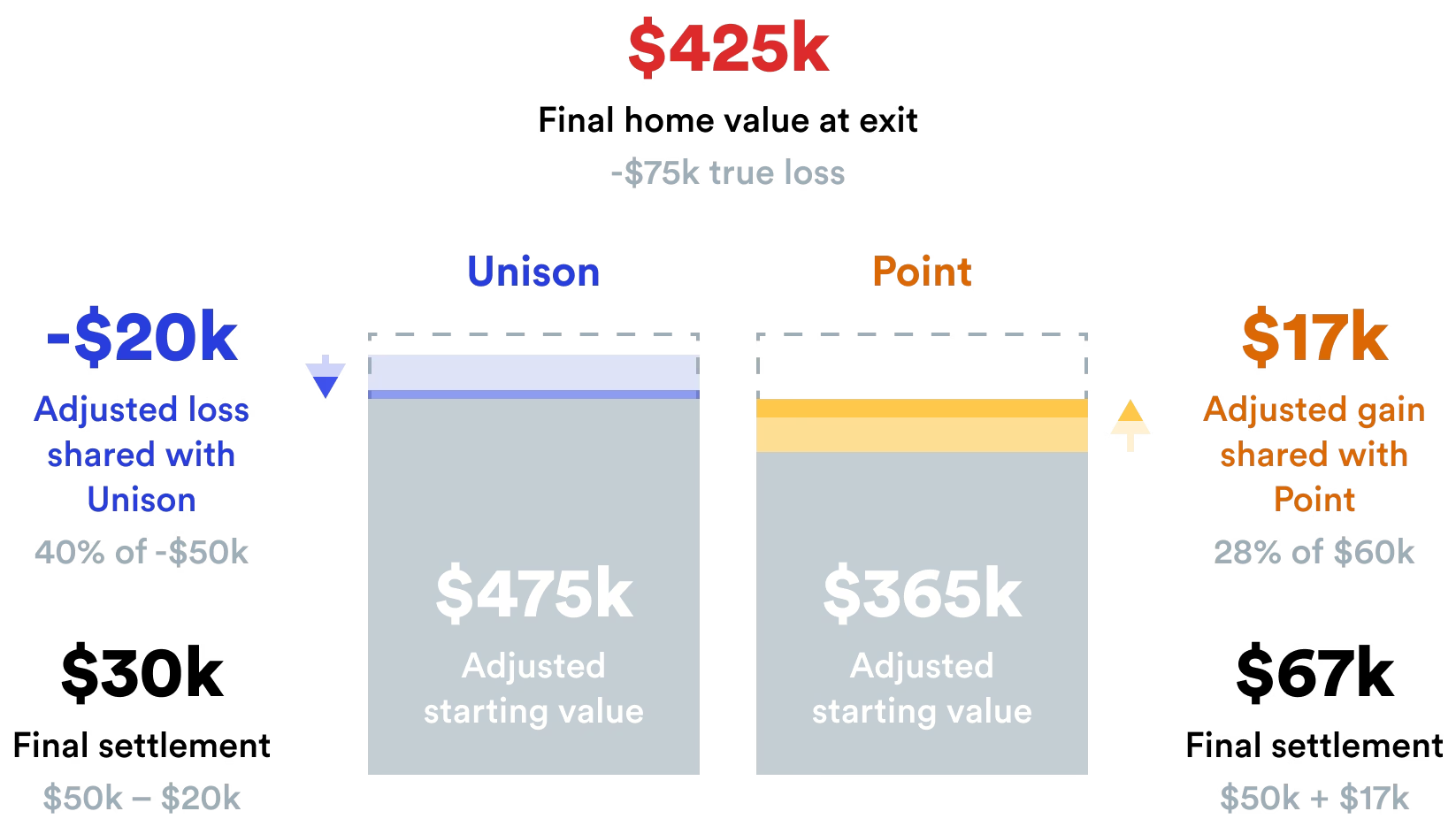

Because this is intended to be a long-term agreement, Unison can’t share in any downside right away. Typically, after the first three years, we share in any loss from a home sale below the Original Agreed Value, reducing what you may owe. And during that initial restriction period, we place an Equity Appreciation Limit. That caps our maximum return in the early years to help protect you and keep it fair.

Unison works with homeowners in stable situations

Home equity investment can be offered to homeowners with lower credit scores who have fewer options available. That represents greater risk for providers like Point. They offset that with a large risk adjustment, protecting their investment at the homeowner’s cost. Problem is, even more qualified homeowners end up paying the same price.

Unison, on the other hand, works exclusively with homeowners in more stable positions. We take on less risk, and immediately pass those savings on to you in the form of a reduced risk adjustment.

Unison maintains among the highest credit and underwriting standards in the industry, including a FICO score minimum of 620. Unison is A+ rated with the Better Business Bureau, has been featured in USA Today, Forbes, and other publications, and we’ve now helped 10,000+ households across 29 states.

Unison vs. Point: The Key Differences

Frequently asked questions

How long is the term and what happens at the end?

You can use the funds provided by Unison for up to 30 years. At the end of this term, you will need to either sell your home or buy us out.

If you’re interested in buying Unison out of the agreement, please review the “Can I buy out Unison’s investment in my home?” FAQ for more information.

In some cases, after 30 years it might be possible to refinance your home and use the proceeds to buy out Unison's investment. However, there is no guarantee that this option will be available.

How does Unison determine my home's starting value?

If both you and Unison accept the value from your appraisal, we will then reduce that value by a 5.0% Risk Adjustment. The resulting value is called the Original Agreed Value. This 5.0% adjustment to your home’s appraised value helps account for the uncertainty inherent in the appraisal process. It also allows Unison to deliver your funds faster and without the added costs of multiple appraisals.

Original Agreed Value = Appraised Value - 5.0%

For example, if your home has an appraised value of $500,000, your Original Agreed Value will equal $475,000.

Does Unison share in the downside if my home loses value?

Yes. Unison is not a loan; we are invested in your home alongside you, so we win and lose together. Though such cases are not common, with significant decline in your home’s value–something neither of us are looking for!–it is possible that the value of the agreement, and your ending amount due to Unison, would be $0. It’s this feature along with the absence of any monthly payments that distinguishes an equity sharing agreement from a loan.

Will Unison share in the value of my home improvements?

We believe that if you make improvements to your home (beyond regular maintenance) that boost its value, you should get all the benefits. That’s why we use a tool called a Remodeling Adjustment.

To qualify for a Remodeling Adjustment, you need to work with licensed contractors and fully document the project. We then use an independent appraiser to determine how the work changed the value of your home, making sure you receive full benefits. Keep in mind that some renovations add more value than others and some don’t add any new value at all. Whenever you are thinking about a project it is always a good first step to reach out to our team. It’s important to note that the Remodeling Adjustment doesn’t apply if you end the agreement in the first three years.

What are the costs associated with Unison?

For the Unison equity sharing agreement, Unison will deduct a 3.9% transaction fee from your agreement at closing.

Additionally, you are responsible for third-party costs such as appraisal and settlement costs (including title, state taxes, and recording fees). Appraisal fees generally range from $450 to $1,250, home inspection fees typically range from $650 to $1,050 and settlement costs range from $700 to $1,750, depending on your area. Your exact costs will be provided to you prior to closing.

In addition to our standard 3.90% transaction fee, customers who obtain an equity sharing agreement from Unison are responsible for the cost of their home inspection. (There is no home inspection fee for customers who choose not to work with Unison). If you happen to have a recent home inspection that meets standard criteria, let us know and Unison will consider using that one instead.

If you choose not to work with Unison, you will not be responsible for any fees. Additionally, Unison pays any cost of credit reporting, as applicable.

How is Unison's profit or loss calculated upon sale?

When you sell your home, you'll need to pay us the original amount that we shared with you, plus or minus our percentage of your home's change in value. Unison's percentage depends on how much we invested in your home at the outset.

If you choose to buy us out instead, we'll use an independent third-party appraisal to determine the fair market value of your property at the time. If you buy us out, Unison does not share in any decrease in your home's value.